It is anticipated that by 2026, electric vehicles (EVs) will account for a fifth of all new car sales, the number escalated by the planned ban on the sale of fossil-fuel cars which has been brought forward to 2030. Statistics show that electric car sales increased by 40 percent in 2022 with more than 1 in 10 new vehicles being electric.

With “mainstream” brands such as Audi, Mercedes and BMW introducing all-electric models, and the advancements in battery range, the electric car market has become more appealing to the average household. However, while electric cars sound great in principle, you must weigh up the different pricing elements and the vehicle range (and therefore the practicability), but most of all, if the cars are actually available. It’s not unheard of for individuals to end up waiting over 12 months after placing an order for cars to be delivered.

While electric cars sound great in principle, you must weigh up the different pricing elements and the vehicle range (and therefore the practicability), but most of all, if the cars are actually available

Sources commented in December that there had been a reduction in waiting times for electric cars, but individuals placing orders in January 2023 could still expect a 28-week lead time. However, there appear to be many “deals” on the purchase of electric cars which is a clear sign that there are more cars becoming available in the market. Tesla is one manufacturer that has recently started offering discounts of over £7,000 for those willing to make the switch over.

So, although electric models can have their drawbacks – range and cost being two – it is still worth looking at the tax advantages of electric car ownership which may just even up the playing field.

Company car?

Of course, one of the most appealing options when it comes to EVs is running one as a company car. As with petrol or diesel cars, there is still a benefit-in-kind implication, but as you would expect, the rates are much lower than their fossil-fuel counterparts.

If the electric car is new and unused, the company can claim tax relief on 100 percent of the cost of the car […] that figure is only 18 percent if the car is purchased second-hand

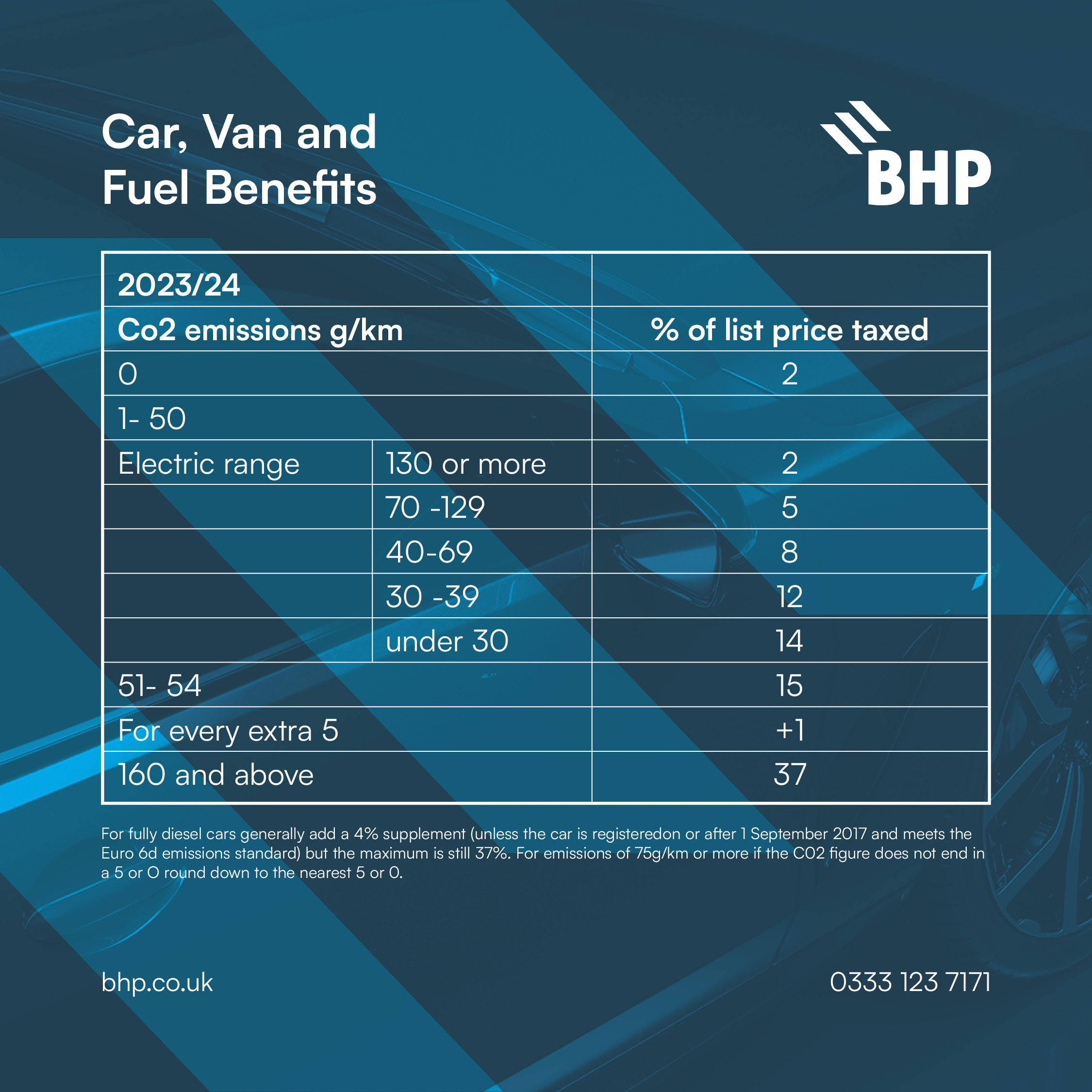

If a fully electric car can be obtained, the employee will still pay income tax on the benefit-in-kind, but this is calculated at the very low rate of only 2 percent of the list price in the 2022-2023 to 2024-2025 tax years (Table 1). The employer’s Class 1A National Insurance contribution (NIC) will be due on this amount so a PAYE scheme will be needed. Additionally, no car fuel benefit applies as tax law does not currently treat electricity as a fuel.

Furthermore, if the electric car is new and unused, the company can claim tax relief on 100 percent of the cost of the car. That figure is only 18 percent if the car is purchased second-hand. All maintenance costs, including insurance, can also be offset against profits.

| Car, van and fuel benefits (2023/24 | ||

|---|---|---|

| CO2 emissions (g/km) | Percentage of list price taxed | |

| 0 | 2 | |

| 1 to 50 | ||

| Electric range | 130 or more | 2 |

| 70 to 129 | 5 | |

| 40 to 69 | 8 | |

| 30 to 39 | 12 | |

| Under 30 | 14 | |

| 51 to 54 | 15 | |

| For every extra 5 | Plus 1 | |

| 160 and above | 37 | |

Not fully electric?

If you can’t quite make the plunge to full electric for whatever reason, it could still be tax efficient to look at a hybrid vehicle where the benefit-in-kind is therefore calculated using the CO2 emissions combined with the electric range. However, you need to remember that for capital allowances purposes, the 100 percent first-year allowances wouldn’t be available and the car would only receive an 18 percent writing down allowance if the CO2 emissions are 50g/km and below.

Charging facilities

Of course, one of the practicalities to consider when owning an EV is having the infrastructure available to charge the vehicle. Many feel that the deadline of 2030 for banning the sale of new fossil-fuel vehicles will not be led by the production of the cars themselves, but the infrastructure being developed to charge the vehicles throughout the country.

Many feel that the deadline of 2030 for banning the sale of new fossil-fuel vehicles will not be led by the production of the cars themselves, but the infrastructure being developed to charge the vehicles

However, if the company can provide workplace charging facilities, then no benefit-in-kind will arise provided these facilities are at or near the workplace, are available to all employees and are for the battery of a vehicle in which the employee/director is either the driver or passenger.

Also, an employer can, for electric company cars, pay for a vehicle charging point at an employee’s or director’s home without a taxable benefit arising. Similarly, a charge card can be provided, without benefit, to allow access to commercial charging points. Alternatively, an advisory fuel rate of 4p per business mile travelled is available. Relief is also available for self-employed business owners against their profits with a restriction for any private use of the vehicle.

Which EV?

To make this more practical, let’s look at three different options from Mercedes-Benz and the benefit-in-kind implications.

First up is the fully electric Mercedes-Benz EQA250, which will be compared against the hybrid Mercedes-Benz C300e with an electric range of 68 miles and a Mercedes-Benz E300 with CO2 emissions of 161g/km. (All cars have models with a list price in the region of £50,000 to £60,000 at the time of writing, so we have used a price list of £55,000 for illustrative purposes.)

| Car | EQA250 | C300e | E300 |

|---|---|---|---|

| Type | Fully electric | Hybrid | Petrol |

| CO2 | n/a | 12 | 161 |

| Electric range | 255 | 68 | n/a |

| List price (£) | £55,000 | £55,000 | £55,000 |

| 23 to 24 benefit-in-kind rate | 2% | 8% | 37% |

| Benefit-in-kind | £1,100 | £4,400 | £20,350 |

| Income tax at 40 percent | £440 | £1,760 | £8,140 |

| Class 1A National Insurance contribution at 13.8 percent | £151.80 | £607.20 | £2,808.30 |

As can be seen from Table 2, there is an income tax saving of £7,700 to be achieved from operating a fully electric vehicle compared to a car with “high” CO2 emissions. On top, the ECQ would also allow the company to claim 100 percent of the cost upfront against taxable profits, while the C300e would be written down at 18 percent per annum, and the E300 at 6 percent per annum based on the CO2 emissions.

There is an income tax saving of £7,700 to be achieved from operating a fully electric vehicle compared to a car with “high” CO2 emissions

For many drivers, that sort of saving would encourage a swap-over. Indeed, evidence is certainly showing a movement towards EVs, but not at a rate that would make motoring journalists think that the 2030 target is still achievable.

Salary sacrifice schemes

A car salary sacrifice scheme is an agreement between the employer and employee to reduce an employee’s salary in return for the use of an electric car.

Salary sacrifice schemes for electric cars can be tax-efficient due to the savings in income tax and NICs and the low benefit-in-kind rates mentioned above. Each month a portion of salary will be automatically deducted, prior to tax, and this will cover the monthly repayment on the car.

Servicing and insurance will typically be included as part of the scheme, leaving the individual to just pay for electricity. Schemes tend to last from two to four years and the cars can be for private or business use.

Final thoughts

There are clearly plenty of potential benefits to owning an electric company vehicle, but the practicalities need to be balanced out between tax, cost and range along with the ability to recharge.

If you are an employer, showing your “green credentials” in the modern world of recruiting by offering an electric car scheme may tip the scales in your favour to obtain the right talent and that should never be forgotten either.

{kind=link}